Ever since the start of the pandemic, central banks across the world have undertaken massive easing measures to support the economy. This could possibly be because of the lessons learned from the 2008 recession. Back during the credit and housing crisis of 2008, the problems were mainly of liquidity and had originated from the housing market of the US.

While the Federal Reserve did take some steps to support the market, these turned out to be too little and too late. As a result, the US and subsequently the global economy was plunged into one of the worst economic crises ever since the depression of the 1930s.

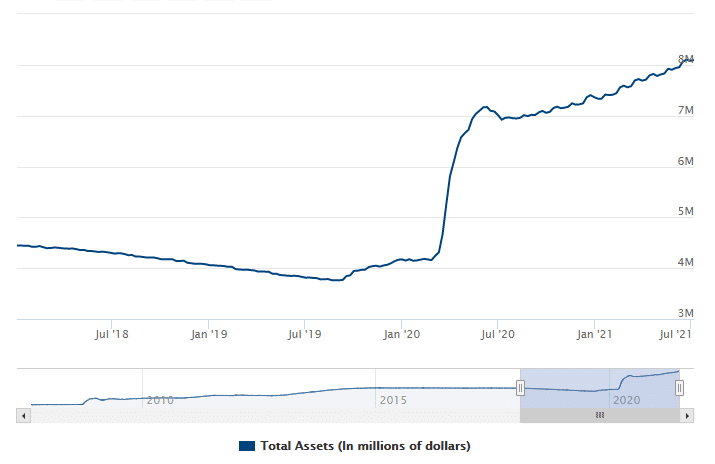

Having witnessed this crisis just a few years back, the Federal Reserve was quick to act this time around. The Fed increased its bond purchases at a record rate, with its balance sheet also seeing a commensurate rise.

As can be seen in the chart above, the Federal Reserve purchased billions of dollars of assets every week in the initial months of the pandemic. It has continued its purchases so far, with the Fed balance sheet now standing at a staggering $8.1 trillion!

Impact of Fed Quantitative Easing in the FX Market

It is obvious that when the central bank decides to pump in such massive amounts of liquidity in the system, it will have ripple effects across all financial markets. In the case of the forex market, the impact was in the form of oversupply. When the Federal Reserve bought huge amounts of bonds, they paid cash for that, which was subsequently pumped into the financial system. This led to an oversupply of the US dollar.

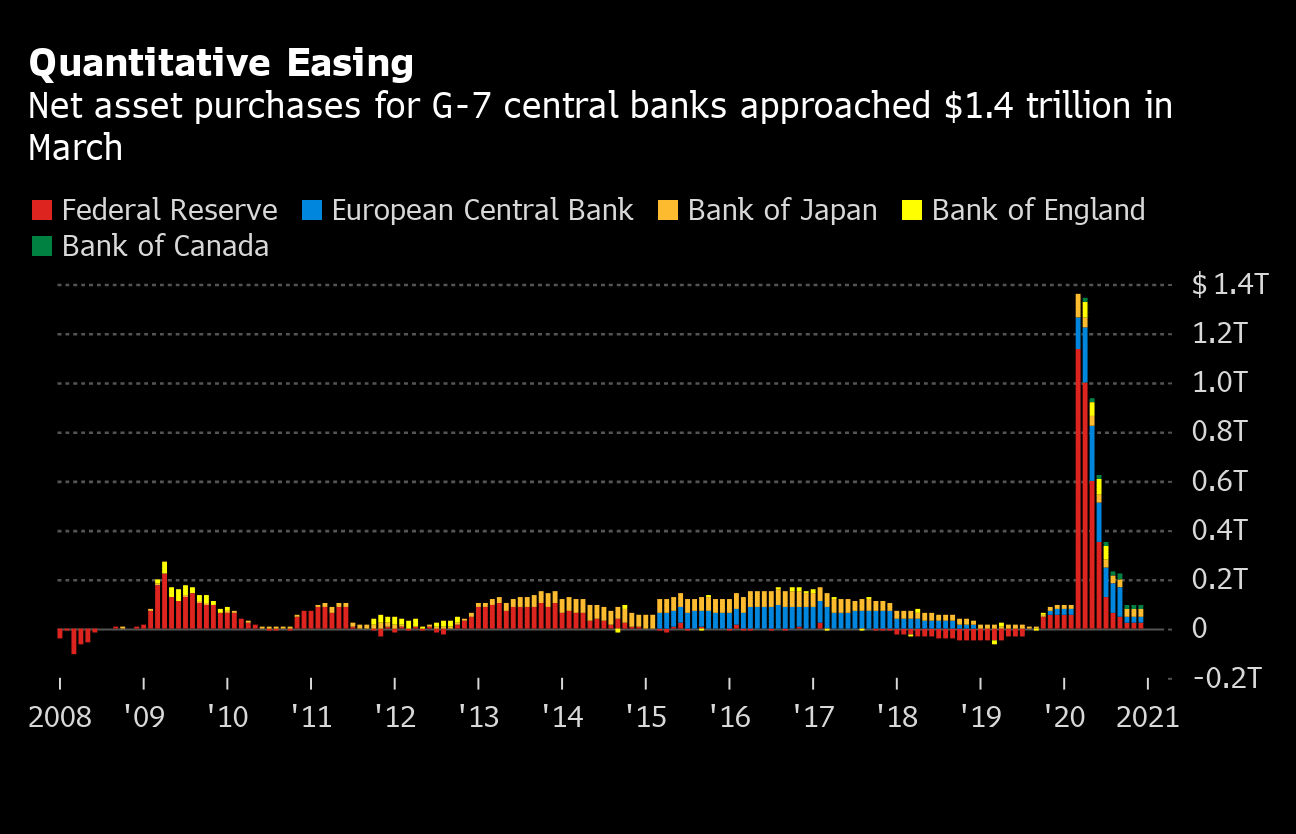

So in the initial phase of the pandemic, the US dollar strengthened because, as a reserve currency, many investors flocked to it. But over the next few months, the dollar saw some depreciation, especially against currencies of developed markets such as EUR, GBP, AUD, CHF, and JPY. This is because the Federal Reserve’s easing measures far outpaced those of other developed nations, as can be seen in the below figure.

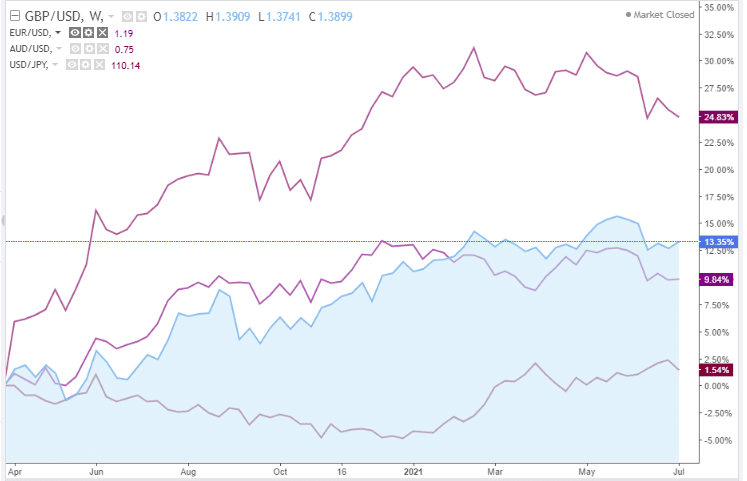

It is very natural that the impact on the FX market will be quite similar, as seen below. Do note that USDJPY seems to have traded in the opposite direction.

That is because the currency pair is defined in terms of the amount of JPY to be paid for 1 USD, while the other currency pairs are defined as vice-versa.

Easing measures unsustainable

It is pretty obvious that changes of this magnitude are not sustainable. Moreover, their purpose might already have been served. The reasoning behind such massive USD pumping was to support the US economy. The US government had put some very stringent restrictions on businesses and individuals in order to control the Covid-19 pandemic.

However, over the past few months, we have seen a sharp recovery of dollar shorts. Vaccination numbers have been picking up, with nearly half of the US population fully inoculated. This has helped the Federal government and state governments to lift restrictions across the country. The reopening is also reflected in the economic numbers, which have been encouraging so far.

Moreover, the US inflation rate has been on the rise as well. For the Federal Reserve, this is a major point of concern. All the economic growth can be undone if inflation goes out of control. Inflation is an obvious side effect of these easing measures. So, keeping all these points in mind, the Federal Reserve has been giving indications that it might start to taper its purchases much sooner than expected.

Now a similar situation had happened in 2013. The Federal Reserve had initiated bond purchases in response to the 2008 crisis, and it had continued doing so for several years. This had made markets complacent who expected surplus liquidity for extended periods. However, in 2013, Ben Bernanke declared his intentions to taper the purchases. This caught the markets by surprise. The US dollar saw a sharp appreciation, and, as a result, nearly all currency pairs saw a massive move in a matter of days!

What lies ahead?

Despite several indications by the Federal Reserve in its FOMC meetings, the markets still don’t seem to have priced in any sort of tapering. FX prices still remain around the same levels as they were before the Fed indicated a change of its intentions. This sets up the market for particularly sharp moves across the board.

Although, unlike Ben Bernanke, Jerome Powell, who is the current Federal Reserve chairman, is known to be much better at communication. He has so far made statements so that they ease the markets into any changes rather than any sudden announcements. But despite multiple statements indicating a potential taper, the markets seem to have ignored it so far.

So, it is a matter of time and patience. There are two paths out there. One is that the Federal Reserve continues to make these statements and make the taper extremely gradual. In this case, even though there will be an initial sharp market reaction, it will not continue for long.

The second case is that the Federal Reserve feels that the purchases are doing more harm than good, especially on the inflation front. In that case, there could be a significant reversal with the Federal Reserve sharply reducing its purchases. Markets are bound to react sharply in this particular case, and the prices will continue to remain impacted for an extended period of time.

This will be acutely felt in emerging markets as they are most sensitive to risk-off measures like this. The previous taper had seen these currencies depreciate by 20-30% and even caused a current account crisis for many countries. Only time will tell which path the Federal Reserve takes, but we should be prepared for an impact on the markets.